By Darren Brown

By wisdom a house is built, and by understanding it is established; by knowledge the rooms are filled with all precious and pleasant riches. Proverbs 24:3-4

One of the most exciting and emotional process that any person will go through is that of buying a house. Taking the leap to homeownership can provide a feeling of pride while boosting your long-term financial outlook, more so if you are well-prepared.

Here are a few considerations: –

- Check your financial status – By far one of the most important things to do is to determine your financial status. Understanding what you own versus what you owe. Looking at possibly any assets and identifying what can be easily converted to cash. Importantly, what is your income source, and how well is it meeting your current needs? Can it accommodate more debt? Are you servicing well any debt you have now?

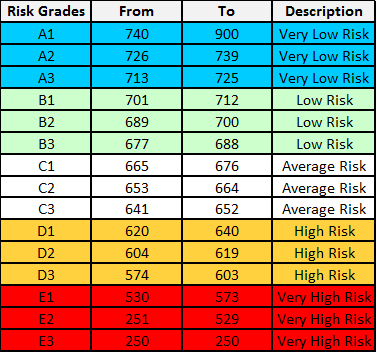

- Do a credit check – this will identify your creditworthiness based on your score as a consumer. Credit score plays a key role in a lender’s decision to offer credit. It is used to evaluate the probability that an individual will repay loans in a timely manner. The higher the score, the better a borrower looks to potential lenders. A credit score is based on credit history: number of open accounts, total levels of debt, and repayment history, and other factors. Every Jamaican over the age of 18 is entitled to receive a free copy of their credit report each calendar year. See – www.crif.com.jm or www.creditinfojamaica.com or www.credit.cisjamaica.com

- Save your deposit – It’s ideal to have enough money to pay the deposit on your home. Perhaps you should look at having at least 10 percent of the price of the house to make that deposit. Many people find that they are not able to buy a house because they are not able to make the deposit although they earn enough to make the monthly mortgage payments. On the other hand, various institutions knowing the challenges that confront persons in relation to these costs will consider incorporating same in the mortgage based on certain criteria.

- Shop for a mortgage – Affordability is key in determining if a lending institution – a building society, a commercial bank, or the National Housing Trust (NHT) – will lend you money to purchase a house. Currently, mortgage rates vary between institutions. National Housing Trust is the cheapest option for sourcing a mortgage with the lowest interest rate of 5%. The most NHT currently affords an individual to borrow is $6.5 million to buy on the open market or to “build on your own land”. Borrowing more would require joining with another qualified contributor, thereby potentially doubling the sum that can be borrowed.

- Secure legal guidance – Generally, it is advisable to engage the services of an attorney-at-law to handle matters such as drafting the sales agreement and ensuring that your legal rights are protected. You will also incur costs for the valuation of the property, surveying, stamp duty, transfer tax and registration; greater clarity for all of these will be provided by your attorney.

- Hiring a real estate agent – An experienced real estate agent can save you time and money by helping you find your ideal house and by negotiating with the seller on your behalf.